By Colin Wright - Uspire Chair

A passionate coach and mentor, Colin has a belief that knowledge and experience should be shared to enhance the lives and success of others.

Colin is a former Managing Director of Vodafone, Caudwell Group, Greencore and Hazelwood Foods.

It was Rachel Reeves second big moment in the spotlight, the first Spring Statement from the UK’s first female Chancellor of the Exchequer, delivered on 26 March 2025. The House of Commons, buzzing with anticipation, listened as Reeves laid out Labour’s economic vision in a statement that balanced fiscal restraint with strategic ambition. Against a backdrop of slowed growth, stubborn inflation, and rising borrowing costs, the Chancellor’s message was clear; prudence now, productivity later. Gone were the rhetorical flourishes of previous years, instead, Reeves adopted a tone of sober clarity, speaking less like a politician with a red box and more like a Finance Director reviewing a fragile P&L.

The statement’s top-line revision came from the Office for Budget Responsibility (OBR), which trimmed the UK’s 2025 growth forecast from 2% to just 1%, a decision likely to ripple through markets and ministerial inboxes alike. While some hoped for stimulus, Reeves focused on trimming and tightening. £4.8 billion will be shaved off welfare spending by 2030, defence received a £2.2 billion boost, and overseas aid was reduced to 0.3% of gross national income, raising eyebrows at the Foreign Office. In a more technocratic twist, the Chancellor also pledged increased investment in HMRC to crack down on tax fraud and projected £6.8 billion in gains through planning reforms expected to unlock over 1.3 million new homes.

But beneath the spreadsheets and policy points lies a deeper paradox, a government elected on a mandate for fairness, now balancing its books through cuts to welfare and overseas aid, while encouraging national rearmament and courting the private sector for growth. For some, this signals a shift to “Blair 2.0” economics, fiscally cautious, socially progressive, and tactically aware of market sentiment. For others, it risks falling between two ideological stools, neither bold enough to transform the economy nor conservative enough to reassure jittery investors.

The most contentious measure by far was the reduction of the Universal Credit health element for new claimants, a technical change with very human consequences. Charities and think tanks quickly noted the OBR’s projection that the policy could push an additional 250,000 people, including 50,000 children, into relative poverty by 2029. While Reeves counterbalanced this with a modest rise in the standard allowance over the same period, critics argue the changes hit the most vulnerable at a time of real need.

And what of Labour’s hallmark decision to scrap the non-dom tax regime? Although it plays well with voters, the fiscal fallout is becoming clear. Over 10,800 high-net-worth individuals exited the UK in 2024, costing HM Treasury billions in lost tax revenue. Reeves finds herself in an unenviable position, cutting from the bottom while watching revenue evaporate from the top.

Ultimately, this Spring Statement wasn’t about shock or sparkle. It was a spreadsheet speech, pragmatic, restrained, and perhaps even refreshingly dull. But with growth forecasts slashed, inflation still simmering, and wealthy taxpayers voting with their passports, the UK’s economic equation remains a stubborn one. As Reeves left the dispatch box, she may well have wondered, is balancing the books enough when the table they’re sitting on is still wobbling?

Key Highlights:-

The Office for Budget Responsibility (OBR) revised the UK’s growth forecast for 2025 down from 2% to 1%, citing weaker economic performance.

A £4.8 billion reduction in welfare spending is planned by 2030. This includes a 50% cut to the Universal Credit health element for new claimants, while the standard allowance is set to increase from £92 per week in 2025-26 to £106 per week by 2029-30.

An additional £2.2 billion is allocated to the Ministry of Defence, aiming to invest in new equipment and position the UK as a “defence industrial superpower.”

Investment in HMRC aims to increase prosecutions for tax fraud by 20%, with an expected revenue increase of £1 billion by the end of the decade.

Changes to planning rules are projected to add £6.8 billion to the economy over the next five years and facilitate the construction of over 1.3 million new homes.

Overseas aid is reduced to 0.3% of gross national income, saving £2.6 billion by 2029.

Critical Assessment

The Spring Statement reflects a focus on fiscal consolidation through significant spending cuts and strategic investments. The welfare reforms, particularly the reduction in the Universal Credit health element, are expected to save £4.8 billion but have raised concerns about increasing poverty levels. The OBR estimates that these cuts could push an additional 250,000 people, including 50,000 children, into relative poverty by 2029-30.

The increased defence spending aligns with a strategy to bolster national security and stimulate economic activity through the defence sector. However, the effectiveness of this investment in achieving broader economic growth remains to be seen.

The planning reforms aimed at boosting housing construction are ambitious and could have positive long-term economic impacts. Yet, the success of these reforms will depend on effective implementation and overcoming potential bureaucratic hurdles.

The reduction in overseas aid has been met with criticism, as it may affect the UK’s international standing and commitments to global development.

Bank of England’s Perspective

The Bank of England (BoE) has maintained the base interest rate at 4.5%, with considerations for potential rate cuts later in the year due to economic uncertainties. Governor Andrew Bailey acknowledged the challenges of balancing a stagnating economy, a weakening job market, and persistent inflationary pressures, which are projected to rise to 3.75% later this year.

Economic Think Tanks’ Reactions

The Institute for Fiscal Studies (IFS) noted that in response to deteriorating global economic conditions, Chancellor Reeves adjusted spending plans to adhere to fiscal rules. The IFS highlighted that the Bank of England’s interest rate is expected to remain higher for longer, indicating ongoing economic challenges.

The National Institute of Economic and Social Research (NIESR) revised its growth expectations for the UK economy down to 0.8% for the year, attributing this to inflationary pressures, uncertain external demand, and tighter monetary policy.

Alternative Approach Focused on Stimulating Growth

A strategy could have involved a more balanced approach between spending cuts and revenue generation. Implementing progressive taxation measures, such as increasing taxes on higher income brackets or introducing new taxes on wealth, could generate additional revenue without disproportionately impacting lower-income individuals. This would classically be a historical labour government approach to solving spending deficits.

However, since the Labour government assumed power in 2024, the United Kingdom has experienced a notable exodus of high-net-worth individuals (HNWIs). Specifically, a net total of 10,800 millionaires left the UK in 2024, marking a 157% increase compared to the previous year. This equates to approximately one millionaire departing every 45 minutes.

Impact on Tax Revenues

The departure of these HNWIs has significant fiscal implications. According to the Adam Smith Institute, each millionaire contributes, on average, £393,957 annually in income tax. Consequently, the exodus of 10,800 millionaires is comparable to the tax contributions of approximately 529,200 average taxpayers.

The Office for Budget Responsibility (OBR) had projected that abolishing the non-domiciled tax status would generate an additional £2.5 billion annually over five years. However, this estimate may not have fully accounted for the potential outflow of wealthy individuals. Oxford Economics warns that if even a quarter of non-doms leave, the UK could lose billions in tax revenues, investment, and philanthropy.

In summary, the migration of HNWIs from the UK since the Labour government took office represents a substantial loss in tax revenues, investment capital, and philanthropic contributions, potentially impacting the broader economy.

If the exodus of HNWIs is directly related to the non-dom reforms or broader Labour tax policy, the UK could end up £8.75 billion worse off over five years than if it had left the non-dom regime unchanged and retained those individuals.

The estimated additional tax losses over five years, beyond income tax, due to the exodus of high-net-worth individuals is approximately £9.57 billion. This includes losses from capital gains tax, dividend tax, stamp duty, and VAT. You can view the detailed breakdown in the table provided. Let me know if you want to model different assumptions or include philanthropic and investment impacts.

Unquantified losses from:-

Spending in UK businesses and services

Philanthropic donations and investments

Longer-term loss in entrepreneurial activity and job creation

This non-dom policy is increasingly looking like a poor financial decision.

To invigorate economic growth, the government could consider the following strategies:-

Accelerating infrastructure projects, such as transportation networks and digital connectivity, can create jobs and enhance productivity. For instance, the proposed expansion of Heathrow Airport aims to operationalise a third runway by 2035, potentially boosting economic activity.

Investing in research and development, particularly in sectors like artificial intelligence and clean energy, can position the UK as a leader in emerging industries. The government’s plan to invest £500 million over two years to fund artificial intelligence innovation centres is a step in this direction.

Implementing comprehensive training programs to upskill the workforce aligns with the evolving demands of the job market. Initiatives like the construction training package to train up to 60,000 workers support this objective.

Simplifying planning regulations can expedite business operations and infrastructure development. The government’s support for reforms in pension legislation to unlock over £100 billion in corporate pension surpluses for broader economic investments exemplifies this approach.

Investing in regional projects, such as the Oxford-Cambridge growth corridor, can stimulate local economies and reduce regional disparities. Accelerating the development of homes and transport networks in this area could add £78 billion to the economy by 2035.

Cuts to the Government civil service overhead

The figures below are a clear indication that AI and productivity challenges could save significant amounts from the government budget.

In the United States, public sector employment as a share of the total workforce is lower than in many European countries, but Trump and Musk are keen to reduce this further using Germany as a benchmark of best practice.

Public Sector Employment in the USA

Overall Percentage (2023–2024):-

Roughly 13.6% of the U.S. labour force is employed in the public sector. This includes federal, state, and local government workers.

(Source: U.S. Bureau of Labour Statistics & World Population Review)

Comparison with Europe

USA: ~13.6% of workforce in public sector

UK: ~18.1%

France, Nordics (e.g. Norway, Denmark): ~25–30%

Germany: ~11–12%

EU Average: ~16–18%

The UK figure whilst better than France, Spain, Italy and the

Interest Rates and Monetary Policy

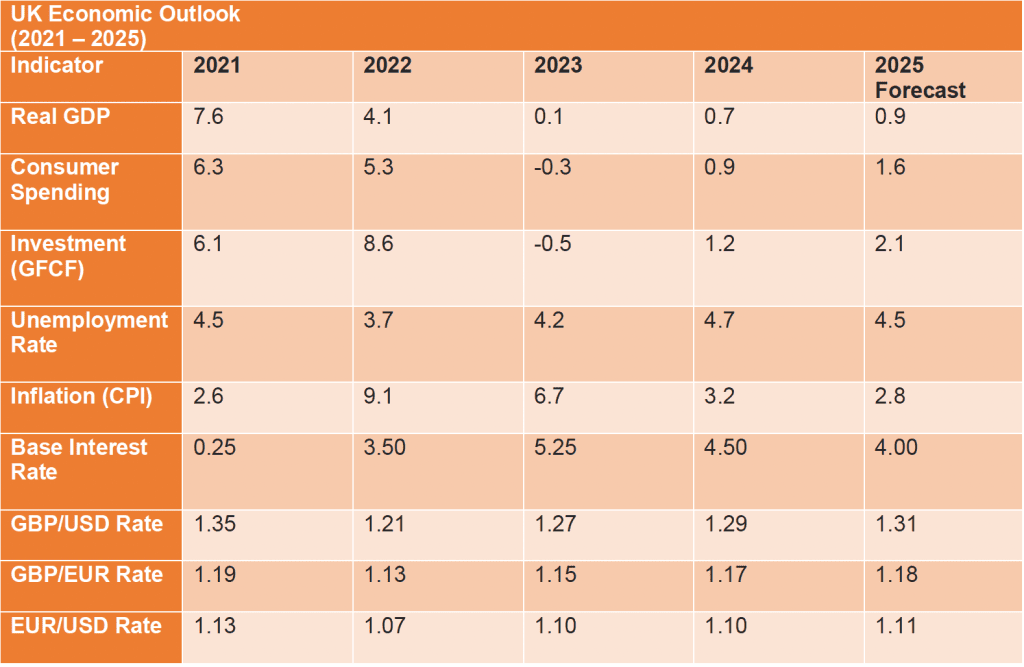

We cannot get away from the fact that the Bank of England's monetary policy stance remains a crucial factor in shaping the UK's economic trajectory in 2025. After the aggressive rate-hiking cycle of 2022-2023, the consensus among analysts points toward a gradual easing of monetary policy. Goldman Sachs projects the Bank rate to settle at 4.25% by end-2025, down from its peak of 5.25% in late 2023.

The Monetary Policy Committee (MPC) has indicated in its forward guidance that rate cuts will be data-dependent, particularly focusing on wage growth and core inflation metrics. Barclays Capital forecasts the first rate cut to come in Q2 2025, with potential for two to three additional cuts through the year, contingent on inflation remaining within target range.

HSBC's UK economist notes, "The pace of monetary easing will be measured and cautious, reflecting the BoE's commitment to ensuring inflation expectations remain well-anchored. We expect a terminal rate of 4% by year-end 2025."

Inflation Outlook

Inflation expectations for 2025 show continued moderation from the elevated levels seen in previous years. The Bank of England's Quarterly Bulletin projects CPI inflation to average 2.3% in 2025, approaching but slightly above the 2% target. Core inflation is expected to prove more sticky, with services inflation particularly resistant to rapid decline.

Deutsche Bank's research team suggests, "While headline inflation should continue its downward trajectory, underlying price pressures, particularly in the services sector and wage growth, will prevent a rapid return to the 2% target. They forecast average inflation of 2.4% for 2025."

Our opinion will be closer to 3% because of the labour on costs that are driving price increases particularly in the food and hospitality sector.

Key factors influencing the inflation outlook include

GDP Growth and Economic Activity

The UK's economic growth prospects for 2025 reflected a gradual improvement from the subdued performance of recent years. The Office for Budget Responsibility (OBR) only two months ago forecasted GDP growth of 1.8% for 2025, while private sector estimates range from 1.5% to 2.2%.

Morgan Stanley's European economics team projects, "We expect the UK economy to expand by 1.9% in 2025, supported by recovering real incomes, lower interest rates, and improved business investment as policy uncertainty diminishes." These now look too optimistic.

Key growth drivers include:-

However, structural challenges persist, including productivity growth limitations and Brexit-related trade frictions. The National Institute of Economic and Social Research (NIESR) highlights that potential output growth remains constrained by these factors.

Housing Market

The UK housing market in 2025 is expected to show signs of stabilisation after the adjustment period triggered by higher interest rates. Nationwide Building Society forecasts house price growth of 2-3% for 2025, reflecting improved affordability as mortgage rates decline and wage growth continues.

Halifax's housing economist notes, "The market is likely to find a new equilibrium in 2025, with transaction volumes recovering from the subdued levels of 2023-24. We expect price growth to remain modest but positive, supported by the fundamental supply-demand imbalance in the UK housing market."

Key housing market indicators:-

Office for National Statistics (ONS) data shows:-

Rightmove's analysis indicates that the ratio of average house prices to average earnings remains elevated at 6.8x, though this varies significantly by region:-

The Bank of Mum and Dad and Joint Mortgages

The "Bank of Mum and Dad" remains a crucial market force, with UK Finance reporting parental contributions reaching £8.6 billion annually in property purchases. According to the Building Societies Association, excess household deposits now stand at £145 billion, providing substantial potential support for first-time buyers.

Joint mortgages have become even more prevalent, with UK Finance data showing they now represent 85% of all new mortgage approvals. This trend is particularly pronounced among first-time buyers, where joint applications account for 90% of approvals. The average combined household income for joint mortgage applicants has reached £75,000, according to Santander's latest mortgage market review.

Currency Markets - Sterling, Euro, and Dollar

Sterling's performance in 2025 is expected to be influenced by monetary policy differentials and broader economic fundamentals. JP Morgan's FX strategy team forecasts GBP/USD to trade in the 1.28-1.32 range through 2025, with potential for higher levels if UK economic performance exceeds expectations.

Against the euro, sterling is projected to maintain relative stability. Credit Suisse forecasts an EUR/GBP range of 0.84-0.87, reflecting convergence in monetary policy between the UK and Eurozone.

Key currency factors:-

Household Finances - Income, Debt, and Savings

Household financial health is expected to show improvement in 2025, though challenges remain for certain segments of the population. The Resolution Foundation projects real disposable income growth of 1.5% in 2025, marking a welcome relief after the cost-of-living pressures of recent years.

Disposable Income

Bank of England analysis suggests that falling inflation and continued wage growth will support real income recovery. Average weekly earnings are forecast to grow by 4.5% in nominal terms, translating to real income gains as inflation moderates.

Household Debt

The Financial Conduct Authority (FCA) anticipates household debt levels to stabilise in 2025, though concerns persist about the impact of higher interest rates on mortgage borrowers. Total household debt-to-income ratios are expected to remain elevated at around 140%.

PwC's economic analysis notes, "While aggregate household debt levels remain high by historical standards, lower interest rates and improved income growth should help ease servicing pressures for many households in 2025."

Savings

The savings ratio is projected to normalise around 8% in 2025, down from the elevated levels seen during the pandemic but above pre-pandemic averages. Deloitte's consumer tracker suggests continued caution in household spending and saving behaviour, reflecting lingering economic uncertainty.

Government Borrowing

The UK's fiscal position in 2025 continues to reflect the challenges of high public debt and ongoing spending pressures. The OBR forecasts public sector net borrowing to decline to 3.2% of GDP in fiscal year 2025/26, though this remains above pre-pandemic levels.

Key fiscal metrics:-

Debt-to-GDP ratio projected at 98% by end 2025

Interest payments expected to consume 8% of tax revenues

Structural deficit estimated at 2.5% of GDP

Government Bond Market

The gilt market outlook for 2025 suggests relatively stable conditions, with yields expected to moderate as monetary policy eases. RBC Capital Markets forecasts 10-year gilt yields to trade in the 3.25-3.75% range through 2025.

Citi's rates strategists’ comment, "We expect gilt yields to trend lower through 2025 as the BoE easing cycle progresses, though term premiums are likely to remain elevated given high issuance needs and global rate dynamics."

Stock Market Outlook

The UK equity market outlook for 2025 reflects improving domestic conditions and global market influences. The FTSE 100 is expected to benefit from its international exposure and value characteristics, while mid-cap indices may see stronger performance as domestic economic conditions improve.

UBS equity strategy team projects, "We see potential for the FTSE 100 to settle at 8,200-8,500 by end-2025, supported by attractive valuations, strong dividend yields, and improved corporate earnings growth."

Sector outlook:

Labour Market and Employment

The UK labour market in 2025 is expected to maintain relative strength, though with some moderation from the tight conditions seen in recent years. The Bank of England forecasts unemployment to settle around 4.5% by end-2025, representing a slight increase from current levels but still historically low.

Key labour market trends:-

KPMG's employment outlook suggests, "The labour market should remain relatively tight in 2025, though with greater balance between supply and demand. Skill shortages in technical and professional roles will continue to drive wage pressures in specific sectors."

Trump Administration Impact on UK Economic Outlook

The return of Donald Trump to the White House marks a significant shift in the global economic landscape that will impact the UK's economic trajectory in 2025. Market analysts are rapidly adjusting their forecasts based on policy signals and diplomatic developments.

Immediate Market Response

JP Morgan's Global Markets Strategy team observes, "Financial markets are pricing in increased volatility as policy uncertainty rises. The immediate focus is on trade relations, particularly regarding China and the EU, with potential spill over effects for the UK."

Key market reactions include:-

Trade Policy Dynamics

US-UK Relations

The prospect of a bilateral US-UK trade agreement has returned to focus. Citigroup's analysis suggests, "While Trump has historically favoured a UK trade deal, his administration's emphasis on reducing trade deficits could complicate negotiations. The UK's trade surplus although low compared to most Country’s in services with the US may become a point of contention."

Trump’s Economic Intervention - The Antithesis of Process Control

In the field of manufacturing, Statistical Process Control (SPC) is a disciplined method that emphasises minimal intervention, accurate measurement, and a deep understanding of variability within the system. The goal is to make small, incremental adjustments that maintain process stability and yield predictable outcomes. This philosophy is rooted in respect for system complexity, recognising that overcorrection or excessive tinkering often introduces more problems than it solves.

Central banks such as the Federal Reserve and the Bank of England traditionally embrace a similar philosophy in their approach to economic management. Interest rate adjustments tend to be incremental rather than abrupt. Policymakers closely monitor indicators like inflation, employment, and GDP growth, acknowledging the delicate interplay between different economic variables. The aim is to steer the economy gently, making course corrections without causing unnecessary disruption to the broader system.

Donald Trump’s economic management style diverges sharply from this model. Rather than subtle, data-driven adjustments, his administration favoured dramatic, often impulsive interventions. These aggressive shifts, such as sudden tariff implementations, sweeping tax reforms, and abrupt immigration restrictions, exemplify a “dial-turning” approach, in which multiple economic levers are pulled simultaneously with little regard for system interdependencies.

Moreover, Trump’s economic policies frequently pursued contradictory objectives. While he sought to reduce immigration as a core political goal, he simultaneously demanded a revival of domestic manufacturing and a resurgence of industrial jobs. These aims conflict at a structural level, particularly given the labour demands of modern manufacturing.

The Labour Market Paradox

Goldman Sachs Economic Research has illuminated the paradox at the heart of this policy strategy. On one hand, the U.S. manufacturing sector is projected to require between 3 to 4 million additional workers by 2030 to meet production goals and replace an aging workforce. The median age of a manufacturing worker in the U.S. is already around 45, and technological advancements are driving the need for higher-skilled labour in areas such as precision engineering, robotics, and automation.

On the other hand, the administration’s policy to reduce immigration has significantly constrained labour supply growth. Estimates suggest that annual labour force growth could fall from 0.5% to just 0.1% if current immigration trends persist. This sharp decline in skilled labour availability could result in productivity losses upwards of $500 billion annually, further intensifying pressure on an already strained sector.

The economic costs of such a shortfall are significant. Wage inflation is likely as employers compete for a shrinking talent pool. Meanwhile, firms may be forced to accelerate investment in automation, increasing capital expenditures at a time when international competitors benefit from more flexible labour policies. The combined effect could be a decline in global competitiveness and a renewed wave of offshoring, ironically, the very outcome the policy was designed to prevent.

Systemic Intervention: A Mechanical Analogy

Managing an economy is much like maintaining a finely tuned industrial machine. Traditional approaches, akin to process control in engineering, involve small, thoughtful interventions based on real-time feedback and a thorough understanding of system dynamics. This methodology favours stability and predictability.

By contrast, Trump’s approach resembled a technician turning multiple dials to their extremes without fully grasping the machine’s internal mechanisms. This kind of intervention increases the likelihood of destabilisation. Without synchronisation or system, wide understanding, the result is often unpredictable and potentially catastrophic. Just as with a machine, aggressive and simultaneous adjustments in a complex economy can trigger unintended chain reactions and eventual breakdown.

Complexity economics offers a helpful lens for understanding these dynamics. In this view, economies are not linear systems but adaptive networks where small inputs can yield outsized, often unpredictable effects. Their interconnected nature means that interventions must be carefully calibrated. Radical, broad-spectrum policy changes introduce systemic risks, particularly when feedback mechanisms are ignored or misunderstood.

Econometric Conclusion

The current Trump policy configuration serves as a textbook case of systemic mismanagement. By simultaneously constraining labour supply and increasing demand for skilled labour, the U.S. risks undermining its own industrial revival. The result is a likely increase in production costs, a drop in competitiveness, and diminished economic resilience over time.

Ultimately, economic dials cannot be turned aggressively in multiple directions without serious consequences. Precision, patience, and a systemic understanding remain the only reliable tools in navigating complex economic terrain.

Late Bulletin “Liberation Day”

President Donald Trump’s recent “Liberation Day” announcement introduced a sweeping set of tariffs, including a universal 10% duty on all imports to the United States, with significantly higher rates for specific countries, 34% on Chinese goods, 24% on Japanese products, and 20% on imports from the European Union. The United Kingdom faces a 10% tariff on its exports to the U.S., a comparatively moderate rate resulting from intensive lobbying efforts by Sir Keir Starmer.

Potential Impact on Markets and GDP

The immediate response from financial markets has been notably negative. U.S. stock futures experienced significant declines, with the S&P 500 dropping 3.7% and the Nasdaq sliding 4.6%. Oil prices also fell, reflecting investor concerns about potential global economic disruptions.

Economists warn that these tariffs could lead to stagflation, a combination of rising prices and slowing economic growth. The increased cost of imports is likely to raise consumer prices, reducing purchasing power and potentially dampening consumer spending. Furthermore, retaliatory measures from affected countries could harm U.S. exports, exacerbating trade deficits and hindering GDP growth.

While the UK secured a lower tariff rate compared to other nations, the 10% duty still poses significant risks. The National Institute for Economic and Social Research (NIESR) projects that these tariffs could nearly erase the UK’s economic growth, particularly if the EU implements retaliatory tariffs affecting UK exports. Sectors such as automotive and manufacturing, heavily reliant on exports to the U.S., are especially vulnerable.

Our prediction is that Rachel Reeves fiscal headroom will be at least halved by these tariffs and begs the question why this was not considered in the Spring statement.

Domestically, U.S. businesses and consumers are expected to bear the brunt of increased costs due to higher import prices. Industries dependent on imported materials, like automotive and technology, may face higher production costs, potentially leading to job cuts and reduced investment. Additionally, the potential for a full-scale trade war could further destabilise the economy, with trading partners imposing their own tariffs on U.S. goods.

The potential benefits that the Trump administration claim, are speculative and contingent on various factors, including the responses of trading partners and the adaptability of domestic industries. The overall consensus among economists and market analysts leans heavily toward concern over the negative implications of the tariffs.

This analysis and the projections below draw on forecasts and projections from:-

Forecasts and projections should be treated as indicative and subject to revision as economic conditions evolve.